TL;DR

- Not all RWA assets demand the same level of state synchronization. Some require none. Some require only unidirectional observation. Others lose their financial meaning unless on-chain and off-chain succeed together or fail together.

- This research defines the sync degree as a classification axis: the strength of state synchronization an asset requires to perform its financial function. The four-level sync degree hierarchy consists of S₀ (Static), S₁ (Unidirectional Observation), S₂ (Bidirectional Coupling), S₃ (Atomic State Binding). The hierarchy is not a scoring ladder but a reduction relation: a system capable at one degree can safely handle assets at any lower degree, but the reverse does not hold.

- The boundary predicate separating S₁ from S₂ is causal consistency. Whether Lamport‘s happened-before relation binds state transitions across two domains as a single causal unit is the entry condition into S₂. The predicate is defined over (asset, system) pairs, not over assets alone. From this definition, the bidirectional delivery of existing data oracles, structurally composed of two independent unidirectional channels, falls into S₁ by definition.

- The five attributes of the TVO framework are reinterpreted as discrete classifiers placing assets within the sync degree hierarchy. In particular, any asset subject to regulatory action is forced to at least S₃, regardless of other attributes. The nature of regulatory action is that simultaneous application across both domains is required, and absence of that simultaneity produces regulatory arbitrage.

- The sync degree hierarchy operates across three layers. For industry, it provides a classification language for the market and establishes an objective criterion for what counts as bidirectional. For academia, it proposes a classification framework for asset state coupling strength, a sister question to distributed system synchrony models. For the product, it grounds the design rationale of OSS internal routing and pricing track branching.

- The formal proof of hierarchy monotonicity (“higher-degree systems safely process lower-degree assets”) is outside the scope of this research. This research proposes the reduction hierarchy and leaves its formalization to subsequent work.

1. The Space Between Two Extremes Must Be Filled

In our previous research, we formally defined the atomicity of bidirectional state synchronization [1]. The core was the distinction between two extremes. The bidirectional delivery of existing oracles operates through two independent unidirectional channels (two-unidirectional channels), where half-execution, one side succeeding and the other failing, is structurally possible. Atomic state binding, by contrast, binds state transitions across two domains as a single causal unit, where either both sides succeed or both sides fail.

That formalization clarified what must be protected. Yet a new question arises where the formalization ends. Do all assets really require atomic binding?

Intuitively, the answer is no. A static NFT with no maturity or interest does not change state after issuance. An insurance product that only reads external weather data needs only unidirectional observation. The interest payment of a bond requires reflection on both sides, but a slight delay on one side does not immediately break financial function. A regulatory asset freeze, however, produces regulatory arbitrage the moment one side remains unfrozen.

The intuition that different assets require different sync levels must be turned into a classification system. Otherwise, two problems follow. First, if a system processes every asset at the strongest level (atomic binding), unnecessary costs arise. Second, if a system processes an asset below its required level, the financial function itself breaks.

This problem was partially addressed in our OEV analysis [7]. There, the focus was on the behavioral difference between discrete price updates and continuous state synchronization, an analysis that implicitly assumed exactly this: that different assets require different sync levels. Liquidation trades dependent on price feeds require continuous sync, while static NFTs do not. But that analysis did not explicit the classification axis itself.

What this research defines head-on is that classification axis: the strength of state synchronization an asset requires to perform its financial function, the sync degree. This axis is not a scoring ladder but a hierarchy formed by a reduction relation, and that reduction relation is what makes the hierarchy a “degree.”

2. Definition of the Sync Degree

2.1 Four Levels

The sync degree classifies the strength of state synchronization an asset requires into four levels. Each level is defined by the strength of state coupling between state domains D₁ and D₂.

S₀ — Static: No state synchronization is needed. The asset’s state does not change after issuance. Examples: collectible NFTs with no maturity or interest, non-financial tokens with metadata fixed at issuance.

S₁ — Unidirectional Observation: Only one-way observation from one domain to another is needed. The asset reads external values and reflects them in its own state, but the asset’s state changes do not need to propagate back to the external domain. This is the ceiling that existing data oracles reach. Examples: tracker tokens that simply reference an external price index, parametric insurance products settling on weather data in one direction.

S₂ — Bidirectional Coupling: State changes in both domains must reflect one another for the asset’s financial function to hold. State transitions across the two domains must be bound as a single causal unit. Examples: bond tokens whose periodic interest payments must be reflected on both sides, security tokens where off-chain KYC state changes affect on-chain tradability.

S₃ — Atomic State Binding: Both domains must either succeed together or fail together for the asset to retain meaning. Intermediate states where only one domain has changed must be unreachable. This is exactly the position of atomic state binding defined in our previous research [1]. Examples: assets subject to regulatory FREEZE actions, derivative exercises, bond maturity redemptions.

The labels of each degree are ordered by the strength of state coupling the asset requires. As we move from S₀ to S₃, state coupling grows stronger, and so do the properties the system must guarantee.

2.2 The Hierarchy Is a Reduction Relation

The decisive point is that these four levels do not form a scoring ladder. They form a reduction relation. By reduction relation, we mean the following.

A system capable of S₃ synchronization can safely handle S₂, S₁, and S₀ assets. The reverse does not hold.

In notation:

$$S_3 \supseteq S_2 \supseteq S_1 \supseteq S_0$$

Here Sₙ is read as “the set of assets that an Sₙ-capable system can handle.” This one-directional containment relation is what makes the hierarchy a “degree” rather than a “level.”

This distinction is not mere terminology. Descriptive classifications like SAE autonomous driving levels L0 through L5 are labels where the capability set of each level is defined by human convention. The reduction relation is not built into the definition. That an L3 system “safely handles” an L1 asset (a situation requiring only lane keeping) is not a theorem derivable from the definition but a separate claim requiring its own verification.

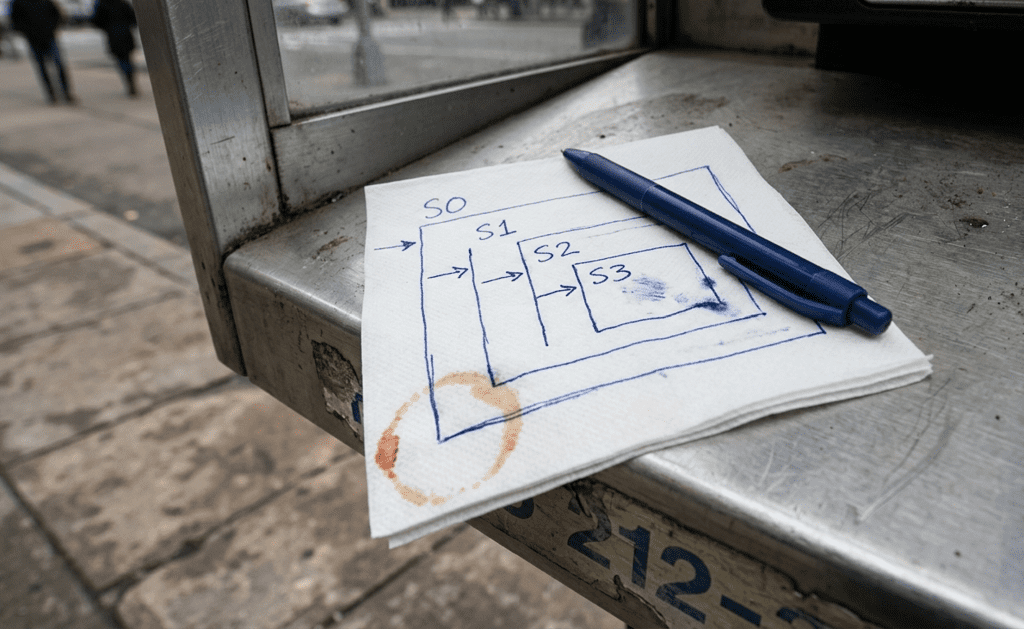

The hierarchy began as four nested rectangles on a napkin, drawn on the edge of a phone booth between two meetings. The one-directional arrow came before the words.

A degree is different. The reduction relation is part of the definition itself, and that a higher-degree system can handle lower-degree assets is the entry condition of the hierarchy. When this one-directional containment closes formally, the degree is elevated from a descriptive label into a proven structure. What that elevation makes possible across industry, academia, and product is addressed in §5.

Figure 1: Sync Degree Reduction Hierarchy

3. The Boundary Predicate Between S₁ and S₂

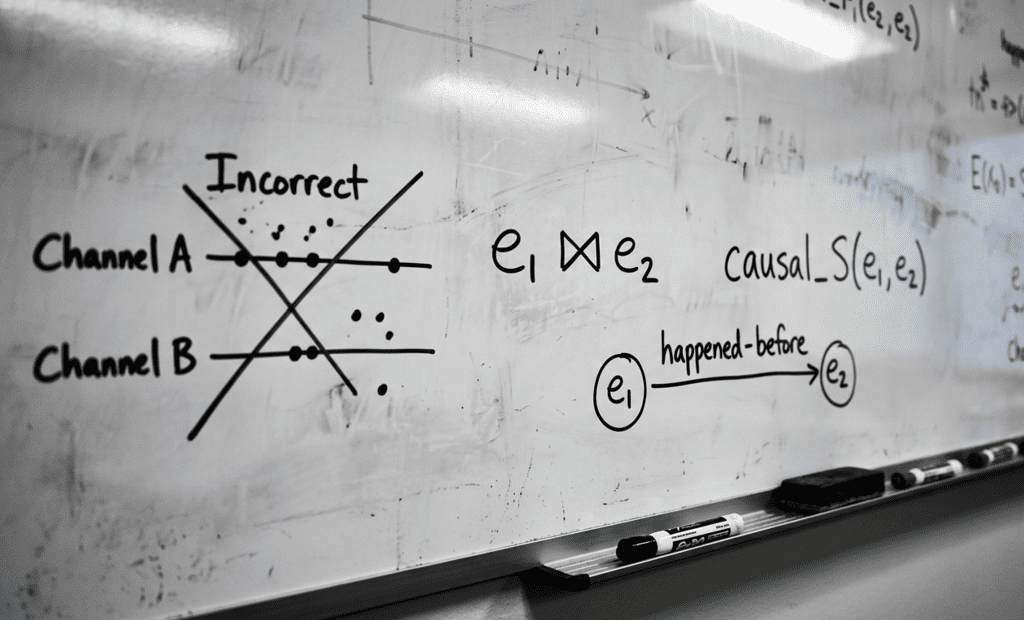

Among the four levels of the hierarchy, the most important boundary is between S₁ and S₂. Where this line is drawn determines whether “the bidirectional of existing oracles” and “the bidirectional of Oraclizer” sit at the same degree or different degrees. Without a formal definition of this boundary, the word “bidirectional” dissolves into a marketing claim.

3.1 The Boundary Predicate: Causal Consistency

We define the predicate separating S₁ from S₂ as follows.

Boundary Predicate: When system S synchronizes asset a, are the state transitions e₁ ∈ D₁ and e₂ ∈ D₂ bound by Lamport‘s happened-before relation [2] as a single causal unit?

In notation, for state transitions e₁ ∈ D₁ and e₂ ∈ D₂:

$$e_1 \bowtie e_2 \iff \text{causal}_S(e_1, e_2) \text{ holds for asset } a$$

Here ⋈ is the mutual causal dependency symbol defined in our previous research [1], denoting that two events are bound as a single causal unit, such that if one does not occur, neither does the other. The predicate causal_S denotes the capability of system S to bind the two transitions as a single causal unit when synchronizing asset a.

- If this predicate holds, system S guarantees synchronization at S₂ or above when processing asset a.

- If this predicate does not hold, the processing of asset a by system S stays at S₁ or below.

3.2 The Predicate Is About (Asset, System) Pairs, Not Assets Alone

A precision adjustment is needed here. The predicate above is not about the asset alone. The asset is an object with requirements, and the predicate is evaluated when a system synchronizes that asset. The sync degree therefore separates into two layers.

The degree of a system: which strength of predicate the system satisfies. The system’s capability.

The degree of an asset: the minimum predicate strength required for the asset to perform its financial function. The asset’s requirement.

To say an asset is “of degree S₂” means: “for asset a to perform its financial function, it must be synchronized by a system that satisfies the causal consistency predicate.” We are not applying the predicate to the asset directly.

If this asymmetry is not made explicit from the start, the model wavers at the very definitional step of subsequent formalization. Formalization tools must define predicates over clearly identified subjects, and the expression “an asset satisfies a predicate” carries no formal meaning.

3.3 Why Existing Oracles Are Capped at S₁

This definition turns one claim into an immediate formal consequence. Existing data oracles, by definition, are capped at S₁.

The “bidirectional” operation of existing oracles consists of two independent unidirectional channels. As shown in our previous research [1], between an event e_A in channel A and an event e_B in channel B, the happened-before relation is not guaranteed.

$$e_A \in \text{Channel}_A, \quad e_B \in \text{Channel}_B \quad \Rightarrow \quad e_A \not\to e_B \;\; \text{and} \;\; e_B \not\to e_A$$

Since the two events are causally decoupled (concurrent), if a system S operates on top of such a channel structure, the boundary predicate causal_S does not hold. Therefore such a system sits at S₁ or below by definition.

“Bidirectional delivery is possible” and “S₂ synchronization is provided” are different claims. Bidirectional delivery capability is the existence of two channels, while S₂ is the strong condition that events across both channels are bound as a single causal unit. Once this difference is anchored in the definition, the marketing claim “we also support bidirectional” can be evaluated as a consequence of the definition.

The boundary predicate took shape on a whiteboard corner one afternoon. The crossed-out two-channel sketch arrived first; the mutual causal dependency symbol came later.

We name no specific project or solution. This is a difference of structural type, and whether a given system falls at a given degree depends on the descriptive accuracy applied to that system’s public specification.

D_on ← Channel B ← D_off

e_A ∥ e_B (concurrent, no happened-before)

capped by structural type

⋈ Bind-Verify-Commit

D_off ─┘

e₁ ⋈ e₂ : mutual causal dependency

happened-before bound as single unit

reached by definition

Figure 2: S₁ Ceiling vs S₃ Position by Structural Type

3.4 Hierarchy Monotonicity Is a Separate Formalization Target

The claim of the reduction hierarchy S₃ ⊇ S₂ ⊇ S₁ ⊇ S₀ contains a separate proposition: monotonicity. The proposition is “higher-degree systems safely process lower-degree assets.” This monotonicity is not self-evident.

Consider, for example, an S₂ asset processed by an S₃ system (one providing atomic state binding). The S₃ system binds two domains with a lock and forces both to succeed or fail together. The S₂ asset requires both sides to be coupled, but whether mutual rollback on simultaneous failure is mandatory is not specified in the asset’s requirements. The simultaneous rollback that the S₃ system imposes overfulfills the S₂ asset’s requirements. Does this overfulfillment harm the asset’s meaning?

As another example, when an S₂ system processes an S₁ asset (which requires only unidirectional observation), the S₂ system forces a causal coupling across two domains. The S₁ asset only needs one domain to change, but the system’s processing imposes a coupling the asset did not require. Is this imposition safe?

Intuitively, it appears safe. The principle that strong guarantees do not break weak requirements is the general principle of overfulfillment safety. But the guarantee that this intuition holds in every case requires a separate formal proof. This monotonicity proof is outside the scope of this research and enters the review territory of subsequent work.

This research states the reduction hierarchy at the level of a proposal. Closing monotonicity formally is a separate subsequent step.

4. TVO Attributes as Discrete Classifiers

How do we place assets within the sync degree hierarchy? Answering this requires a classifier that inspects asset attributes. The five attributes of the TVO (Total Value Oraclized) framework serve this classifier role.

4.1 Reinterpreting the TVO Attributes

The TVO framework measures an asset’s state synchronization dependency S_i as a continuous weight from 0 to 1. The five attributes are assigned weights and summed to derive how much the asset depends on oracle infrastructure.

A note on notation. The sync degrees S₀, S₁, S₂, S₃ of this research use numeric subscripts to indicate position in the hierarchy, while the TVO dependency S_i uses an index subscript to refer to asset i. The letter S is reused but the subscript shapes differ, and this research deals only with degrees. Dependency computation is the work of the TVO context.

| Attribute | Meaning |

|---|---|

| Periodic Payments | Does the asset have periodic interest, dividend, or similar payments? |

| Variable Rate Linkage | Is the asset linked to an external benchmark such as SOFR? |

| Maturity Existence | Does the asset have a maturity? |

| Regulatory Action Subject | Is the asset subject to regulatory action? |

| Off-chain System Integration | Is the asset integrated with off-chain systems? |

This research uses the same five attributes differently. Not as a continuous weight but as a discrete classifier deciding where among S₀ through S₃ to place the asset. The same attribute set served as a quantitative measure of dependency in the TVO context; in the sync degree hierarchy context, it serves as a qualitative classifier determining which degree the asset belongs to.

This reinterpretation is not merely a change of expression. When the perspective of sync infrastructure design shifts from how much it depends to what coupling strength it requires, the same attribute set does different work.

4.2 The Mapping Decision Table

Which combinations of the five attributes map to which degree? This research proposes the following decision table. Evaluation proceeds top to bottom in sequence, and the first matching row determines the final degree.

| Order | Condition | Degree |

|---|---|---|

| 1 | Regulatory Action Subject applies (regardless of other attributes) | At least S₃ (Binding) — forced |

| 2 | One or more of Periodic Payments, Maturity Existence, or Off-chain System Integration (bidirectional reflection required) | S₂ (Coupling) |

| 3 | Only Variable Rate Linkage, with no need for bidirectional reflection | S₁ (Observation) |

| 4 | None of the five attributes apply | S₀ (Static) |

The sequential evaluation rule matters because of combination cases. For instance, “a bond paying periodic interest and linked to an external benchmark” satisfies both Periodic Payments and Variable Rate Linkage. Under sequential evaluation, row 2 matches first and the asset is classified as S₂. The S₁ condition of “Variable Rate Linkage alone” applies only when no other bidirectional-reflection attribute is present.

The first row of the table is decisive. Any asset subject to regulatory action is forced to at least S₃, regardless of the other four attributes. The basis of this forced rule is the nature of regulatory action addressed in our previous research [1, §4.1].

When a regulator issues a FREEZE order, if one domain is frozen while the other remains active, the asset trades freely through the unfrozen channel during that temporal gap. This constitutes regulatory arbitrage, violating the FATF Travel Rule [6] and national AML regulations. “Pending application” is not legally a frozen state.

Therefore, assets subject to regulatory action lose financial function the moment simultaneous application across both domains is not guaranteed. This is precisely the definitional condition of S₃ atomic state binding. Regardless of any other attribute (periodic payments, variable rate linkage, maturity, off-chain integration), being subject to regulatory action alone sends the asset directly to S₃.

4.3 The Rationale for the Other Rows

The S₀ row: If none of the five attributes apply, there is no reason for the asset’s state to change. The asset is static after issuance, and no synchronization is needed.

The S₁ row: Variable Rate Linkage alone, with no need for the asset’s state to propagate back to the external domain. Reading an external benchmark and reflecting it in the asset’s state is sufficient; the asset’s state changes do not need to be reflected in external systems. This fits exactly the definition of unidirectional observation.

The S₂ row: One or more of Periodic Payments, Maturity Existence, or Off-chain System Integration is on. What these attributes share is the need for mutual reflection between the two domains. When a bond’s interest is paid, it must be distributed to on-chain token holders (off-chain → on-chain), and ownership changes from on-chain trades must be reflected in the off-chain rights registry (on-chain → off-chain). When the reflection in both directions is causally bound, the asset’s financial function holds.

One note here. Whether assets satisfying the three S₂ attributes also require atomicity (S₃) varies by asset. A bond’s interest payment may tolerate some delay, while precise maturity redemption may sit closer to atomicity. Detailed analysis of the strength difference between S₂ and S₃ is addressed in subsequent research. This decision table proposes classifying assets as S₂ based on the criterion of “whether bidirectional reflection is required,” and the sub-region where mutual rollback on simultaneous failure is mandatory is then further classified as S₃.

4.4 The Practical Meaning of the Mapping

What does this decision table actually do? Two things.

Provides a decision rule for asset classification: When an asset is tokenized, applying its five attributes to the decision table yields the asset’s sync degree. The degree can be recorded as metadata at the moment of tokenization. The asset registration procedure of OracleMint can include this classification step.

Provides the input to system processing path decisions: Once an asset’s degree is determined, it becomes the input deciding which processing path the asset should take. How this input directs internal routing within OSS, and how that routing closes as compile-time enforcement, is addressed in §5.3.

Figure 3: TVO Attribute Decision Flow Mapping to Sync Degree

5. What the Sync Degree Builds

We have addressed the definition of the hierarchy, the boundary predicate, and the classification mapping. The final question that must be addressed is this: what does this classification axis actually build? A classification is, in itself, only a label. What matters is what the label does. The sync degree does different things at three layers. For industry, it becomes a classification language. For academia, it becomes a classifiable framework that can be closed. For the product, it becomes an enforcement structure.

5.1 Industry: A Classification Language for the Market

Until now, assets in the RWA market have been classified along two axes: value (TVL) and kind (bonds, real estate, commodities, carbon credits, and so on). Both axes address what the asset is, not what it demands from sync infrastructure.

This omission imposes costs on real market decisions. Even within the category “bond token,” a bond whose state does not change between issuance and maturity differs entirely from a bond that may be subject to regulatory freeze in its sync requirements. When an issuer chooses a tokenization platform, when an investor assesses asset risk, when an infrastructure provider sets pricing, there was no language to distinguish this difference. As a result, the market had to either process every asset by the strongest sync requirement (overcost) or by the weakest one (broken financial function).

The sync degree hierarchy provides the market with that language. An S₁ asset and an S₃ asset are different terms. A system capable of S₂ assets and a system capable of S₃ assets are different systems. When the degree is recorded as metadata at issuance, it operates as the first indicator by which market participants view assets.

There is a side effect here. An objective criterion for the word “bidirectional oracle” emerges. Until now, any system with bidirectional data delivery capability could call itself “bidirectional,” and the market had no tool to filter that claim. As shown in §3.3, the definition of the sync degree hierarchy structurally distinguishes “two independent unidirectional channels” from “bidirectional coupling bound as a single causal unit.” Plugging any system into that definition determines its degree. Information asymmetry in the market shrinks.

5.2 Academia: A Classification Framework for an Adjacent Field

Academically, the hierarchy sits adjacent to but distinct from distributed system synchrony models. The Dwork-Lynch-Stockmeyer partial synchrony model [3] and the subsequent synchrony classifications address network assumptions. How messages arrive, whether message delays are bounded, whether nodes operate synchronously. These concern the environmental conditions of distributed consensus protocols.

The sync degree hierarchy addresses a different question. The state coupling strength an asset requires to perform its financial function. It is a sister question to synchrony models, but not the same question. In the same partially synchronous environment, a system processing S₁ assets and one processing S₃ assets must guarantee different properties.

This sister question proposes a formal classification framework in an adjacent new field. If the hierarchy is closed formally, that framework accumulates as an academic asset, becoming a building block other research can cite and reuse. The hierarchy of this research opens the possibility of playing, in RWA asset classification, the role that Lochbihler‘s ADS_Functor [4] played in Canton‘s authenticated data structures.

The lineage of inspiration for this hierarchy, we acknowledge plainly, originates from the Turing degree of Turing’s oracle machine [5]. The Turing degree established a hierarchy through a reduction relation in the domain of computability. If one problem reduces to another, they belong to the same degree, or one stands higher than the other. The sync degree brings the same structural intuition into the domain of asset synchronization. Calling it a “Turing-degree-grade theory” would be overstatement, but the lineage of the intuition is academically honest to cite.

5.3 Product: The Structure of Enforcement

On the Oraclizer product side, the sync degree operates as enforcement. Whether classification stays as a mere label or becomes a structure that blocks incorrect processing inside the system is a decisive difference.

The correctness of OSS internal routing: Once an asset’s degree is determined, it determines which processing path the sync request should take. An S₁ asset takes a lightweight unidirectional observation path. An S₃ asset takes the full BVC (Bind-Verify-Commit) [1] cycle. An incorrect routing — an S₃ asset accidentally entering the S₁ path — leads directly to atomicity violation. An asset subject to regulatory freeze applied to only one domain, or a bond maturity redemption executed on only one side, are the consequences.

When hierarchy monotonicity is closed formally, this routing correctness can be made into type-system-level enforcement. The asset’s degree and the processing path’s degree are compared at compile time, and if the asset degree is higher than the path degree, the compile itself is rejected. Incorrect routing becomes a compile rejection, not a runtime accident. This is structurally different from marking the degree with a mere enum. A mark is a label. A formalized hierarchy is enforcement.

The design basis of pricing track branching: In a separate area, the degree becomes the basis of pricing structure. S₀ assets (no sync needed) naturally fit per-call pricing, since calls are either absent or one-time. S₂ to S₃ assets, where continuous state synchronization happens within an Oracle Session, naturally fit session-based prepaid pricing. The key is that this branching happens not at billing time but at the transaction entry structure of the wallet. Depending on which degree an asset belongs to, the wallet transaction handling the asset either takes the path of a normal chain transaction or that of an Oracle Session initiation request.

That the design basis of this branching can be answered with “it follows from the definition of the degree” is the practical value of a formalized classification axis. “Why does this asset go to the session track?” becomes a consequence of the definition, not a marketing decision.

The formal closure of the hierarchy is possible because its core piece is already in place. The cross-domain state preservation homomorphism [1, §6] proven in our previous research already guarantees the core of S₂ through S₃ (state preservation under bidirectional coupling, identity preservation under atomic binding). Formalizing hierarchy monotonicity is not a new independent verification but the work of laying the reduction relation on top of existing verification assets.

The timing and concrete progression of that work fall outside this research. What this research has addressed is the definition of the classification axis, and what that axis can build at the three layers of industry, academia, and product.

6. Boundaries and Limits

We clarify the boundaries of the sync degree hierarchy this research proposes.

It is a classification axis limited to the RWA and oracle domains. The hierarchy classifies the strength of state synchronization an asset requires to perform its financial function. It is not the work of rewriting distributed system synchrony theory (closed synchronous / partial synchrony / asynchronous models, and so on). This hierarchy is about RWA asset classification, and the tools used to formalize the hierarchy sit on top of existing distributed system theory.

The definition of the degree can be defended through formalization, but the classification of any specific system depends on the descriptive accuracy of that system’s public specification. The claim “existing oracles stay at S₁” is grounded in the fact that the structural type of those oracles is two independent unidirectional channels. If that fact is misdescribed, the classification is misapplied. This is not a limit of the classification tool but a question of accuracy in applying the tool to a fact.

Hierarchy monotonicity has not been proven in this research. This research proposes the reduction hierarchy and notes the possibility of closing monotonicity formally. Until the monotonicity proof is complete, the reduction relation is an intuitive claim, not a formal theorem.

The strength difference between S₂ and S₃ has not been fully determined in this research. Whether the criterion separating bidirectional coupling from atomic state binding — “whether mutual rollback on simultaneous failure is mandatory” — defines a separate degree by its own predicate or is a strength parameter within S₂ is left to subsequent research. This research proposes it as a four-level discrete hierarchy for now, leaving open the possibility that subsequent research redefines it as two points on a continuum.

7. Open Questions

We summarize the open questions this research leaves behind.

Formal proof of hierarchy monotonicity: Whether the reduction relation S₃ ⊇ S₂ ⊇ S₁ ⊇ S₀ closes as a partial order, and whether hierarchy monotonicity (“higher-degree systems safely process lower-degree assets”) is proven as a theorem. Building on the cross-domain state preservation homomorphism theorem of our previous research, this formalization appears feasible, but its full development is the subject of subsequent work.

Completeness of the classification decision table: Does the mapping table proposed in this research cover all combinations of the five attributes without gaps? How does it handle borderline cases such as “assets with periodic payments but no need for bidirectional reflection”? Formal completeness of the classification decision rule remains future work.

The boundary decision between S₂ and S₃: As noted in §6, whether the strength difference between the two is captured by its own predicate or by a strength parameter. Where that decision lands determines whether the hierarchy itself is a four-level discrete structure or a three-level + strength parameter structure.

Dynamic degree changes for assets: Is an asset’s degree static? Does a bond’s degree shift as it approaches maturity? When an asset is elevated from S₂ to S₃ because a regulatory action is imposed, what are the sync infrastructure implications of that elevation? If a degree can change during the asset’s lifecycle, how is the moment of change aligned with the Oracle Session boundary? This area is addressed in subsequent session lifecycle research.

Refinement of existing oracle classification: The claim that all existing oracles stay at S₁ is grounded in structural type. But some oracles attempt to approximate causal consistency through various mitigation mechanisms (such as retry patterns or Saga compensating transactions). Could these mitigation mechanisms create an intermediate stage like quasi-S₂ between S₁ and S₂? This research leaves this possibility open, with full analysis deferred to subsequent work.

Conclusion

This research has unfolded the space between the two extremes defined in our previous research on atomic state binding [1] (independent unidirectional channels versus atomic state binding) into a reduction hierarchy. The sync degrees S₀ through S₃ classify the strength of state synchronization an asset requires to perform its financial function. The essence of the hierarchy is not a scoring ladder but a reduction relation, and this one-directional containment relation is what makes the hierarchy a “degree.”

The boundary predicate separating S₁ from S₂ is causal consistency. Whether Lamport‘s happened-before relation binds state transitions across two domains as a single unit is the entry condition into S₂. The predicate is defined over (asset, system) pairs, not over assets alone. From this definition, the conclusion follows that the bidirectional delivery of existing data oracles, owing to its structural type of two independent unidirectional channels, stays capped at S₁ by definition.

The TVO attributes are reinterpreted as discrete classifiers placing assets within the hierarchy. In particular, any asset subject to regulatory action is forced to at least S₃, regardless of other attributes. The basis of this forced rule is the nature of regulatory action: if simultaneous application across both domains is not guaranteed, regulatory arbitrage arises.

The sync degree does different things at three layers. For industry, it becomes a classification language for the market, allowing assets to be viewed along the axis of sync requirement strength in addition to value and kind, and providing an objective criterion by which the word “bidirectional oracle” can be judged as a consequence of definition. For academia, it becomes a classification framework for an adjacent new field, closing as a classification axis for asset state coupling strength where distributed system synchrony models address network assumptions. For the product, it becomes enforcement, with the design basis of OSS internal routing and pricing track branching following from the definition of the classification. Classification begins as a proposal, passes through formalization, and closes as enforcement.

The next research addresses how the hierarchy actually operates inside the system. How asset degrees determine internal routing within OSS, how pricing tracks branch by degree, and how hierarchy monotonicity can close as a formal asset. If this research built the hierarchy, the next shows that the hierarchy works.

References

[1] Oraclizer Research. (2026). Atomic State Binding: Formalizing Causal Consistency in Bidirectional Synchronization. https://research.oraclizer.io/atomic-state-binding-oracle-synchronization/

[2] Lamport, L. (1978). Time, Clocks, and the Ordering of Events in a Distributed System. Communications of the ACM, 21(7), 558-565. https://amturing.acm.org/p558-lamport.pdf

[3] Dwork, C., Lynch, N., & Stockmeyer, L. (1988). Consensus in the Presence of Partial Synchrony. Journal of the ACM, 35(2), 288-323. https://groups.csail.mit.edu/tds/papers/Lynch/jacm88.pdf

[4] Lochbihler, A., & Marić, O. (2020). Authenticated Data Structures as Functors in Isabelle/HOL. FMBC 2020. https://www.isa-afp.org/entries/ADS_Functor.html

[5] Turing, A. M. (1939). Systems of Logic Based on Ordinals. Proceedings of the London Mathematical Society, s2-45(1), 161-228. https://doi.org/10.1112/plms/s2-45.1.161

[6] Financial Action Task Force (FATF). (2021). Updated Guidance for a Risk-Based Approach for Virtual Assets and Virtual Asset Service Providers. https://www.fatf-gafi.org/en/publications/Fatfrecommendations/Guidance-rba-virtual-assets-2021.html

[7] Oraclizer Research. (2025). The End of OEV: Oracle State Synchronization as the Ultimate Solution. https://research.oraclizer.io/the-end-of-oev-oracle-state-synchronization-as-the-ultimate-solution/